An interesting account of the current cost climate of the Contract Hire market.

I wanted to understand a little more in general about how fleets are managed accross the board and the findings are positive. If you have a business that wants an assist to the bottom line then we can help. If you're already doing a great job we can still help!

This blog is a post about who we are and what we as a company have as our aims and goals.

What's going on in the world of diesel engines? It would seem that governments throughout the world are taking action against them. I don't have an issue with the governments taking action to make the world a cleaner place

, the challenge comes for me when the ones tasked with it's management appear to look at the revenue streams

they can open, driving cold hard cash

into their pockets. What is needed in the UK is a carefully considered framework

, built in full, so that cities around the country can put the model into place for the good of everyone

. Rather than like in some countries who have taxation on clean new diesel engines (as well as old dirty ones)

, but no penalties for old dirty petrols

. If we ultimately want cleaner air

then lets do it the right way

rather than being a bully towards diesels

. It is after all a leading solution for many retail customers as well as businesses

throughout the UK. If the taxation rests on the shoulders of diesel engines

, small and medium business will have to consider the impact of this within their business model, especially the high mileage businesses

.

Another issue I have is the way in which the media portrays the diesel engine as a whole. They're building in the nations mind a picture of doom and gloom from such a filthy block . The reality is that diesel engines are cleaner than ever , they are cleaner today than petrol engines from just a handful of years ago. Air quality is improving year on year. We have 70% less NOx levels to those we saw 30 years ago , and this will continue to improve as older engines come off the road. The media is a money making machine at heart, we all know that, but I feel as though they have a duty to at least provide it's viewers with honest, informed and correct information, this currently does not happen.

Let's face it the investment that manufactures drive into their euro 6 diesel blocks is phenomenal and they are reducing the co2 levels all the time, so much so that it is still better value to run a diesel engine for a company car with the low CO2 and BIK rates . There are 12 million diesel vehicles on the road today and that has been driven by the government and economy. People are still buying them today and will do tomorrow and the day after...

So, what will happen moving forward ? Well...

We can already note a decline in diesel engines being registered . This shouldn't put you off from a company car point of view . The decline is driven mainly by the retail market and that some are switching to an alternate fuel solution . The demand for diesel is still there and standing strong. It will be around for years to come as it's a great solution vs the rest.

You really need to consider all of the above within your purchase route analysis and decision making rules , as it could have a costly impact on your business if not . If you would like any further advice on the above then simply get in touch with us via the form or at consult@yalsoncc.co.uk or on 01924 677577 .

Another issue I have is the way in which the media portrays the diesel engine as a whole. They're building in the nations mind a picture of doom and gloom from such a filthy block . The reality is that diesel engines are cleaner than ever , they are cleaner today than petrol engines from just a handful of years ago. Air quality is improving year on year. We have 70% less NOx levels to those we saw 30 years ago , and this will continue to improve as older engines come off the road. The media is a money making machine at heart, we all know that, but I feel as though they have a duty to at least provide it's viewers with honest, informed and correct information, this currently does not happen.

Let's face it the investment that manufactures drive into their euro 6 diesel blocks is phenomenal and they are reducing the co2 levels all the time, so much so that it is still better value to run a diesel engine for a company car with the low CO2 and BIK rates . There are 12 million diesel vehicles on the road today and that has been driven by the government and economy. People are still buying them today and will do tomorrow and the day after...

So, what will happen moving forward ? Well...

- Scrappage scheme for diesels... maybe.

- Used car diesel prices to steepen their curve of depreciation

... for sure (it's already happening).

- Larger diesel cars impacted less from depreciation alterations ... I would think so.

- Legislation brought in for used diesel engines, especially euro 5... maybe.

- A used car market driven by leasing companies ... definitely.

- Diesel engine popularity decline ... most definitely.

We can already note a decline in diesel engines being registered . This shouldn't put you off from a company car point of view . The decline is driven mainly by the retail market and that some are switching to an alternate fuel solution . The demand for diesel is still there and standing strong. It will be around for years to come as it's a great solution vs the rest.

You really need to consider all of the above within your purchase route analysis and decision making rules , as it could have a costly impact on your business if not . If you would like any further advice on the above then simply get in touch with us via the form or at consult@yalsoncc.co.uk or on 01924 677577 .

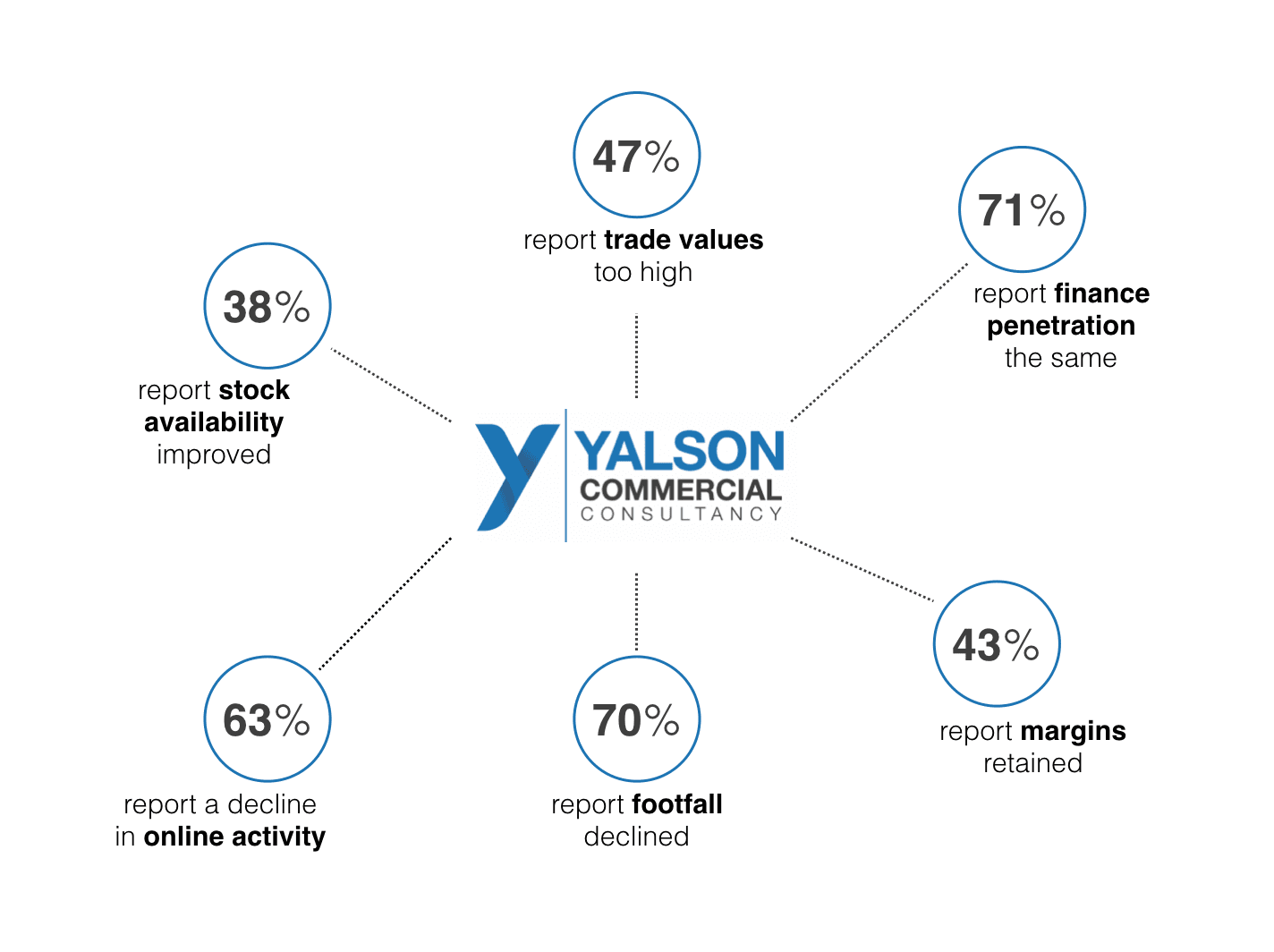

70% of dealers have reported on a decline in footfall

compared to 49% last year. However the dealers noting an increase rose to 16% from 10% the year before.

Online activity performs at a similar level to the physical footfall with 63% of dealers indicating a drop . In 2016, this figures was at nearly half of this year's at 34%. Dealers noting an increase in activity over the month into April dipped to 10% compared to 22% in 2016.

Those offering reports of an increase in margin on the previous month rose to 18% vs 14% in April last year . Conversely, the percentage of dealers who felt they has experienced further compression increased from 25% in April 2017 to 39% in April 2017 . 43% said they experienced little or no change since March.

38% are reporting better stock availability since last month, which is a drop by over one fifth from 59% last year. 26% said stock availability had worsened since March.

Finance penetration seems to be much of the same story as last year, with a fifth reporting a decline this month . Those enjoying an increase fell from 20% this time last year to just 8% this year. Dealers reporting little or no change rose from 58% to 71%.

It looks like the alteration in VED rates has played a part for a declining April vs April 2016. The market just a few days before the end of the month was suffering with reports of a 42% decline on sales year on year . The figures then dramatically changed on the last day of the month . What is this down to? Well it's simple, the same old trick of pre-registrations which is dealers registering stock in their own name for the benefit of target achievement . This means you may see tremendous influxes of certain models within the market place as dealers try and offload this stock. Look out, there may be some deals to be had !

Online activity performs at a similar level to the physical footfall with 63% of dealers indicating a drop . In 2016, this figures was at nearly half of this year's at 34%. Dealers noting an increase in activity over the month into April dipped to 10% compared to 22% in 2016.

Those offering reports of an increase in margin on the previous month rose to 18% vs 14% in April last year . Conversely, the percentage of dealers who felt they has experienced further compression increased from 25% in April 2017 to 39% in April 2017 . 43% said they experienced little or no change since March.

38% are reporting better stock availability since last month, which is a drop by over one fifth from 59% last year. 26% said stock availability had worsened since March.

Finance penetration seems to be much of the same story as last year, with a fifth reporting a decline this month . Those enjoying an increase fell from 20% this time last year to just 8% this year. Dealers reporting little or no change rose from 58% to 71%.

It looks like the alteration in VED rates has played a part for a declining April vs April 2016. The market just a few days before the end of the month was suffering with reports of a 42% decline on sales year on year . The figures then dramatically changed on the last day of the month . What is this down to? Well it's simple, the same old trick of pre-registrations which is dealers registering stock in their own name for the benefit of target achievement . This means you may see tremendous influxes of certain models within the market place as dealers try and offload this stock. Look out, there may be some deals to be had !

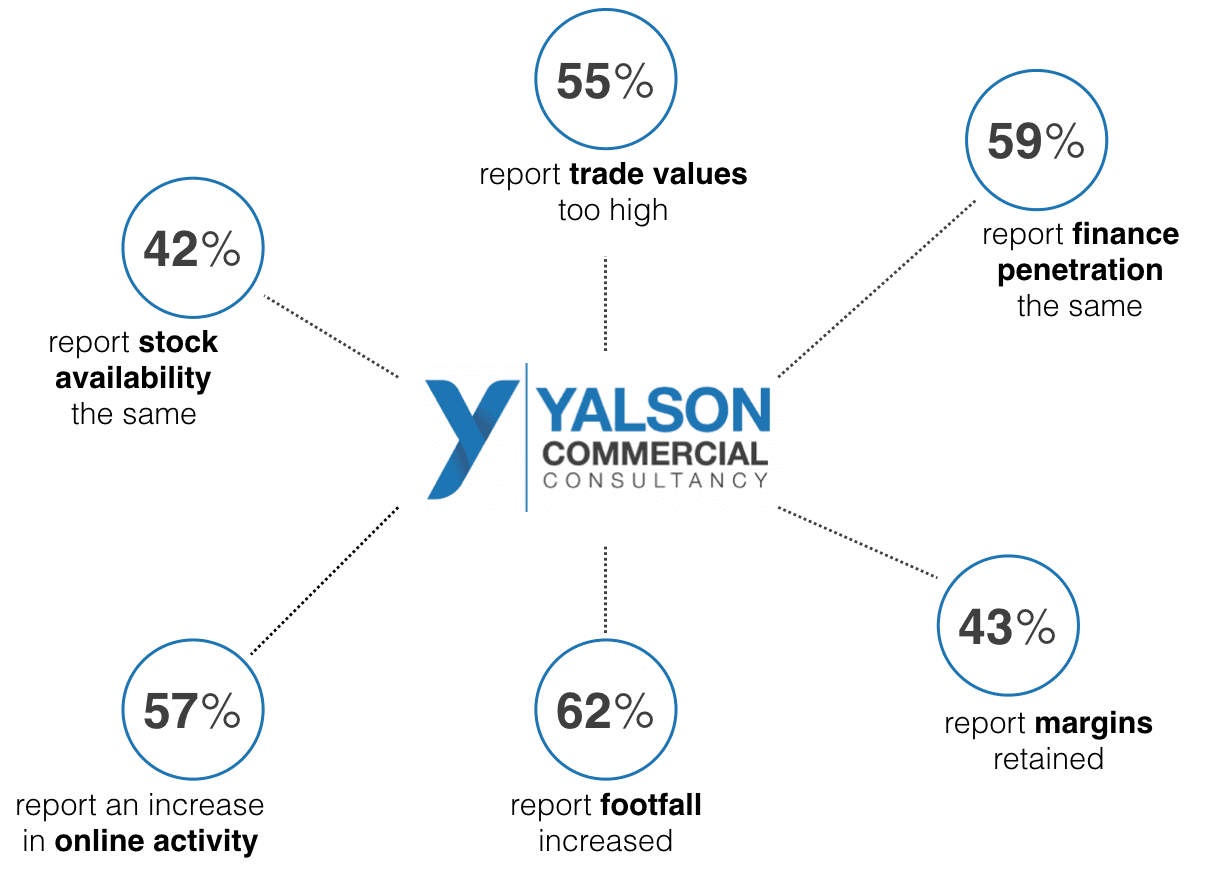

February brings in reports of a 5% decline in the number of dealers seeing an increase in footfall compared to 12 months ago

. The figures are 40% this year with 45% being last years figure

. Dealers reporting a decline rose from 18% 12months ago to 29% this February

. The remaining 31% stated little or no change

.

Online activity follows a similar trend to physical activity for the second month in a row. However, dealers reporting an increase in activity in February were lower than February 2016 - 44% this February vs 53% 12 months ago . Decline is still playing it's part with some dealers, with a rise from 16% shooting all the way up to 27% this year . The dealers reporting tell a story of compression in retained margins jumping from 18% in February 2016 to a huge 39% this year , whilst those informing of an improvement since last month dropped by over half from 28% to 13% . The remaining 48% report on an experience of little or no change since January .

Fast approaching March and just 22% report on an improvement on stock availability since last month, however it is over double the 10% reported last year . Very much the same as last February in that 37% said stock availability worsened since January with the remaining 41% stating no real change .

Finance is the good news story for dealer this February with a report of 37% of dealers seeing an increase with a comparison of 21% in February 2016. 18% indicate a decline since January which is in actual fact a drop of 10% from last year.

There appears to be a steady and controlled rise in most areas. Notice that these are generally percentage increases on the previous year which indicate in increasing activity in many areas.

March is a full concern for dealers now . Like I said last month the early bird catches the worm in this game . Let's see which dealers went strong on their offers and therefore are ahead of the game. Now is the time to push them about to get what we want in terms of the good deals. I certainly know we are pushing them hard at the minute!

Online activity follows a similar trend to physical activity for the second month in a row. However, dealers reporting an increase in activity in February were lower than February 2016 - 44% this February vs 53% 12 months ago . Decline is still playing it's part with some dealers, with a rise from 16% shooting all the way up to 27% this year . The dealers reporting tell a story of compression in retained margins jumping from 18% in February 2016 to a huge 39% this year , whilst those informing of an improvement since last month dropped by over half from 28% to 13% . The remaining 48% report on an experience of little or no change since January .

Fast approaching March and just 22% report on an improvement on stock availability since last month, however it is over double the 10% reported last year . Very much the same as last February in that 37% said stock availability worsened since January with the remaining 41% stating no real change .

Finance is the good news story for dealer this February with a report of 37% of dealers seeing an increase with a comparison of 21% in February 2016. 18% indicate a decline since January which is in actual fact a drop of 10% from last year.

There appears to be a steady and controlled rise in most areas. Notice that these are generally percentage increases on the previous year which indicate in increasing activity in many areas.

March is a full concern for dealers now . Like I said last month the early bird catches the worm in this game . Let's see which dealers went strong on their offers and therefore are ahead of the game. Now is the time to push them about to get what we want in terms of the good deals. I certainly know we are pushing them hard at the minute!

There's some new entries

this year that we have been eagerly waiting on. There are also some interesting and impressive additions to the 2017 family. Right through the range of size and price tag, we've complied a list of our favourites

.

As with everyone, we all have our favourites, and ours is clear. The the all new BMW 5 Series . It's absolutely stunning . It's got the looks , it's got the mechanics , the tech and the gadgets . It would win most comparison tests that it mixes with, from performance to BIK. A word of advice, the 520d M Sport Auto is the sweet spot . Don't get me wrong, if you're car mad and like something a little more underneath the foot then you'll want to dip into the pockets and go for a more powerful engine.

Enough of the 5 Series, here is our list of the new models set to launch in 2017, a list that we think is worth writing home about:

This is by no means a complete list, however, it's the cars we think will have strong residual values in comparison to some of their competition, and certainly to those with predecessors. The cars that are replacements of run out models are born from substantial change, both internally and externally. Future values will be strongly supported by high demand for the early examples of these new models .

As with everyone, we all have our favourites, and ours is clear. The the all new BMW 5 Series . It's absolutely stunning . It's got the looks , it's got the mechanics , the tech and the gadgets . It would win most comparison tests that it mixes with, from performance to BIK. A word of advice, the 520d M Sport Auto is the sweet spot . Don't get me wrong, if you're car mad and like something a little more underneath the foot then you'll want to dip into the pockets and go for a more powerful engine.

Enough of the 5 Series, here is our list of the new models set to launch in 2017, a list that we think is worth writing home about:

- Audi Q2

- BMW 5 Series

- Ford Fiesta

- Land Rover Discovery

- Mazda CX-5

- Mini Countryman

- Nissan Micra

- Peugeot 3008

- Skoda Kodiaq

- Suzuki Ignis

- Vauxhall Insignia

- Volvo XC 60

This is by no means a complete list, however, it's the cars we think will have strong residual values in comparison to some of their competition, and certainly to those with predecessors. The cars that are replacements of run out models are born from substantial change, both internally and externally. Future values will be strongly supported by high demand for the early examples of these new models .

It looks like dealers are revving their engines for a strong first quarter

. Whilst there was a minor dip in the number of dealers reporting a monthly footfall increase in comparison to 12 months ago, 62% of dealers surveyed for 2017 said they experienced an increase in physical footfall

over the previous month, compared to 69% the previous year

. 20% said footfall was about the same

as for December, but encouragingly, this is up in comparison to last year which was at just 17%

.

Online activity follows a similar trend to physical activity. Dealers reported an increase in activity moving into January , however dealers reporting an increase in activity has declined from the previous year.

Stock availability has been recognised as much the same , with 28% reporting an improvement, comparable to the 29% last year. 42% noted little or no change to the stocking levels.

Dealers reporting on their margins remains much the same story as last year, with 33% noting compressed margins in 2017 vs 30% 12 months ago . 43% being the majority commented on little or no change .

Finance penetration results stay inline with last year . 25% report an increase compared to 23% last year . Dealers finance penetration continue to rise off the back of dealer funding incentives and the ever becoming more popular funding route, PCP (Personal Contract Purchase). Manufacturers offer strong incentives, such as deposit contributions which sit strongly with comparable offers of funding. Don't be surprised to see dealers enjoying a strong level of increase with their finance penetrations over the next few years.

There appears to be a steady and controlled rise in most areas. Notice that these are generally percentage increases on the previous year which indicate in increasing activity in many areas. The only area that seems to have stayed much the same is physical footfall. We believe that consumers are educating themselves through the power of the internet before even stepping foot onto a dealers premises.

March is looming for dealers and the momentum will continue to grow into February. I think that the early bird catches the worm in the motor trade and there will be some fantastic deals to be had over the coming months.

Online activity follows a similar trend to physical activity. Dealers reported an increase in activity moving into January , however dealers reporting an increase in activity has declined from the previous year.

Stock availability has been recognised as much the same , with 28% reporting an improvement, comparable to the 29% last year. 42% noted little or no change to the stocking levels.

Dealers reporting on their margins remains much the same story as last year, with 33% noting compressed margins in 2017 vs 30% 12 months ago . 43% being the majority commented on little or no change .

Finance penetration results stay inline with last year . 25% report an increase compared to 23% last year . Dealers finance penetration continue to rise off the back of dealer funding incentives and the ever becoming more popular funding route, PCP (Personal Contract Purchase). Manufacturers offer strong incentives, such as deposit contributions which sit strongly with comparable offers of funding. Don't be surprised to see dealers enjoying a strong level of increase with their finance penetrations over the next few years.

There appears to be a steady and controlled rise in most areas. Notice that these are generally percentage increases on the previous year which indicate in increasing activity in many areas. The only area that seems to have stayed much the same is physical footfall. We believe that consumers are educating themselves through the power of the internet before even stepping foot onto a dealers premises.

March is looming for dealers and the momentum will continue to grow into February. I think that the early bird catches the worm in the motor trade and there will be some fantastic deals to be had over the coming months.

An increasing number of people are turning to the internet for all sorts of advice. Fashion advice. Medical advice. Marriage advice.

Here are Yalson Commercial Consultancy, we certainly won’t dissuade you from getting fashion advice online, but we strongly recommend that you don’t turn to Google for fleet advice, because it could end up costing you a whole lot more than you expected. No one can understand your business at the other end of the internet, without ever having a conversation with you. Advice needs to be considered for each client, then presented in a constructive manner that is tailored and appropriate for that particular client. You can expect nothing less from Yalson Commercial Consultancy.

No one really wants to talk about their depreciating fleet, but this is one business issue you don’t want to leave unattended. After all, it could lead to a major adjustments within the business, adjustments which you are not ready for.

The importance of having a very clear and concise fleet plan takes on even greater magnitude if you have vehicles owned and hired through different purchase routes. Getting expert advice can save you thousands across your fleet and remove the headaches that can come with the understanding of purchase routes and why any particular one should be fitting for your business, let along understanding the period of ownership.